Secondary Commentary: December 2020

Before you read any further, I want to premise with the fact that this is an opinion, MY OPINION, and the intention of it is to help you form an opinion. I don’t have a crystal ball, no direct line to Mr. Powell, President Trump, or President Elect Biden, no insider info, and no magic tweeting power (looking at you Trump) or even know how to tweet. I can’t tell you what is going to happen in 2021 with rates. I can however tell you what happened in 2020 and things to be on the lookout for in 2021

1st Quarter Table Setter

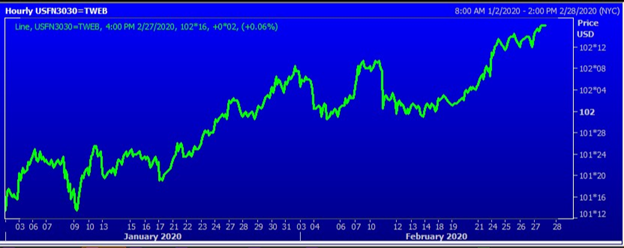

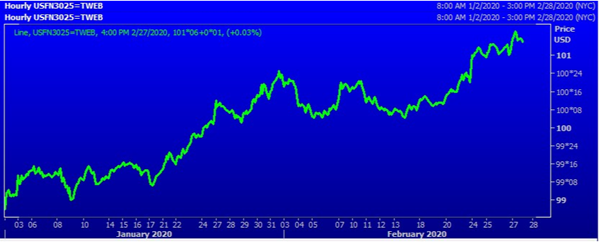

The first quarter of 2020 set the groundwork for what would be a wild ride. We started the year looking at rates in the 4’s. By February we were seeing rates pushing into the mid to low 3s. This was driven by global news of Covid-19. There were fears that this would be a global pandemic and money was flying to safe havens such as US treasuries and UMBS. This sudden lowering of rates caused lock volumes to increase as our past clients became refinance targets.

In the middle of the quarter the Covid fears became reality: a full-on global pandemic had arrived. The low to mid 3s evaporated overnight as Covid-19 appeared on US soil. Rates tanked in a 48hr span and it became impossible to even get a par rate. We sat in this environment for about 7-10 days before the FED stepped in and infused the market with money. This infusion quickly rallied rates back and we say the low 3s appear again. This drove lock volume to 4x normal volumes.

The quarter ended with the FED realizing they infused too much, and they slowly eased their infusion of money. They lowered it to a reasonable range that stabilized the market and set the table for an amazing rate year.

What did this Craziness do to Secondary?

The initial rate rally was easy to handle. We saw an uptick in lock volume and were easily able to adjust our models to account for higher prepay speeds, more renegotiations, and lower pull through. When the market cratered in the middle of the quarter, that is when the fun started in secondary.

Before rates cratered, we could sell 85-90% of our loans to any one of our 12 investors. This is the model we had built over the past several years and what our pricing models were built of off. Our goal was to slowly build a servicing portfolio, while selling most loans to support origination and operational needs. That ability vanished as soon as the global pandemic made its way to the US. In a matter of days, we had investors either stop buying loans, reduce prices to the point we would be selling at a loss, or toss on overlays that were impossible to sell to when we had already underwritten loans.

In the middle of a quarter, we had to scrap our pricing model, scrap our prepay models, scrap our loan execution models…you get where I am going. Basically any model we had was scrapped and tossed back together with band-aids and bubble gum (MacGyver would be proud). We started selling almost exclusively to agencies (Fannie, Freddie, and Ginnie). We as a company are incredibly fortunate to have this ability, as many lenders did not and suffered drastically. We owe a lot of credit to Tom and Jeanie for having the vision to obtain those approvals.

Now for some high-level shi…stuff that may go over your head. When the market has huge swings in pricing, it is a nightmare from a secondary standpoint. When we see large dips and then huge rallies like we did in the middle of Q1, it is a worst-case scenario. In secondary, we hedge our entire locked pipeline – most companies that produce over $500-600mil/yr do the same. What this means is when the market worsens during the life of your lock, we sell the loans at a lower price – but we as a company get a positive pair-off from our hedge, meaning we get money from our Broker dealers. But when the market rallies and we sell loans at a higher price than when the loan was locked, we actually owe our broker dealers money. Well, when you see a 400-700bps rally in the UMBS market, that causes some serious issues. These issues are known as margin calls.

In the midst of everything else that was going on, we were hit with margin calls from just about every broker dealer that we had. It wasn’t just one either, it was multiple – and was a daily occurrence while the market rallied. These margin calls were not a couple hundred dollars either – these were 6 figure margins calls that totaled 7 figures when all was said and done. Luckily, we were able to navigate through this adventure. Every mortgage lender that hedges experienced this. There was a huge outcry from this community when the FED started infusing endless amounts of money, as it pushed some lenders to the point where they couldn’t make the margin calls. This outcry helped to push the infusion of money down to a reasonable level.

While we were in the middle of this margin call mess, we also experienced the single largest lock month in our history, over $400mil in March. As I mentioned, we hedge our entire locked pipeline with broker dealers, but we have a limit with each of them in terms of how much capacity we can hedge. This huge month took us to capacity. We scrambled to find a way to continue locking loans while we reached out to broker dealers trying to get new approvals and line increases. This was a big challenge, as most were not approving new clients and were weary of line increases with the pandemic in full force. We once again got some band-aids and bubble gum out to manage this. We are better for it today, as we now have excess capacity and several more relationships with broker dealers to support origination levels for years to come.

We learned a lot about the department in the 1st Quarter. We navigated the most stressful 45 days of most of our careers in secondary and we SURVIVED!

The Rest of 2020

The first Quarter saw rates in the low 3s, but as the year went on and the pandemic hit the US we saw more little rallies. Lockdowns across the country led to fears of a recession. More and more investors jumped to the safe haven assets, which caused rates to dip lower. The Fed continued to infuse money into the market on a daily basis, which kept stability and allowed for rallies.

As the year has moved on, we have seen rates slowly improve and now have 15 year rates in the low 2s, 30 year rates in the mid to high 2s, and government rates in the high 2s or low 3s. These are interest rates that most people thought they would never see. You have people locking interest rates at or near the FEDs inflation target of 2%.

We did see a few dips in rates for the worse as we started to see the US open back up after shutdowns, unemployment levels come down, and news of vaccines being available soon. Even with this news, the market bounced back each time as news of more Covid cases and more lock downs surfaced. News of on-again and off-again stimulus packages have also moved the market on a weekly or daily basis, but not large swings.

We enter the holiday season with more and more states starting to tighten restrictions on gatherings. We have started to see unemployment levels stop dropping or increase. There are also serious questions about when a vaccine will be available for the masses to help put an end to this pandemic. This uncertainty has caused rates to push to the low levels we see today.

Lock Volumes have remained strong throughout the year as rates remain low. While secondary isn’t locking $400mil/month anymore, we are still 2.5-3 times our normal lock volume for this time of year. With rates at or near their lowest points, we have started to reach the point where people who refinanced at the start of the pandemic are now seeing a benefit from refinancing again. Two refinances in a 12month span… whatever saves the borrower money, right?

What does 2021 bring?

2021 should bring a very strong rate environment for at least the first half of the year. No one knows how long rates will remain at the levels they are at today. There are so many variables at play that no one wants to make these bets. What I can tell you is that the FED remains heavily involved in the UMBS market, and they have not shown signs of easing the amount they are buying. On a daily basis they are buying between $5-7billion in UMBS securities. They have recently started buying 1.5coupon UMBS 30 years which has improved pricing on the lower coupons in the previous few weeks. As long as the FED stays involved, we should see a relatively stable and low rate environment.

The pandemic does not seem to be leaving any time soon. Until we see vaccines readily available and have the population getting vaccinated, we should still see low rates. Until we as a country and we as a global economy can get back to business as usual, we should see a low rate environment. The biggest question hanging over the global economy is what the post-pandemic economy looks like. Many have questioned the length of time it will take to fully recover. The new administration and the FED will play a large role in what post pandemic US Economy looks like.

I wish I had a crystal ball to let you know the exact day/time that rates are going to turn against us. What I would advise is to stay on top of your pipeline and have the lock/float conversations early and often with your borrowers. We are at or near the lowest rate levels in the history of our country, floating for the chance to possibly get .125% lower in rate isn’t always a prudent decision but put that decision in your borrowers’ hands.

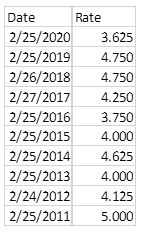

In a write up I did earlier this year, I provided a chart of where rates have been at the end of February for the last 10 years. Below is that chart and a reminder of just how great rates are today. If I were to include a rate for today it would be somewhere around 2.75-2.875%.

Normalization in 2021?

Secondary is hopeful that at some point early in 2021, we can see some normalization in the market. What I mean by this is having our investors fully jump back into the market. Right now, they are only back for A+ paper and are not paying the premiums they once were. As things stand currently, we are still retaining most of our production as we can’t just pool below A+ paper.

We are also hopeful early in 2021 we can get back into doing Jumbos in house, get back to doing Chenoa, and hopefully add a few more DPA programs. The biggest hold up for Jumbos and Chenoa is forbearance. Until we get to the point where borrowers can’t immediately apply for forbearance once a loan closes, it makes it very hard to bring these programs back. Jumbos and Chenoa loans are not saleable once they enter forbearance and can become repurchases if they enter Forbearance too soon after sale. That is a lot of risk to take on, especially when dealing with large loan balances for Jumbos.

Keep Grinding

Most of you have had incredible years. Every time I pull numbers, I am in awe of some of the locked pipelines you all are carrying. Typically, we are entering our slow period for the mortgage industry but this year seems like we might skip past that or have a very brief chance for air. Keep on grinding to the best of your ability. We have all been at this since the start of the year and are in this together. 2020 will be our best year for VanDyk Mortgage, let’s see if 2021 can top it.

Wishing you all a great Holiday season and end of year.

Brad Chatel

Secondary Manager

Secondary Commentary 12.20

Click Start Challenge to begin!