Wait a moment for the newsletter to load, otherwise scroll down to download a copy!

25 Points

Claim Points

Wait a moment for the newsletter to load, otherwise scroll down to download a copy!

March 7, 2023

Sales Fly-In Recap

Sales Fly-In is over, but the memories will last a lifetime. And the glitter probably will too. It got in EVERYTHING! But the sparkle in the eyes of our sales team after hearing from our panelists, hugging their co-workers, celebrating each other’s successes, and learning from one another will last even longer. A brief overview of some main points is below. Look forward to more information soon~

REMINDER – What is available in-house?

In his capacity as National Underwriting Manager, David will use his many years of experience in management, underwriting and problem solving to direct the daily needs of the Underwriting Department, which will include maintaining company service standards, loan quality, productivity, knowledge, training, growth and motivation. David will work closely with Lindsey, Conan, and other management to provide recommendations on escalations/exceptions, process and system improvements, as well as continuing the open line of communication between Sales and Underwriting.

For those who have been with VanDyk for more than a few years, Mary Spirou’s may be a name you know well, and we are happy to announce she will be taking on the new role of Production Support Processing Manager, responsible for the oversight of loans processed under the corporate umbrella and focusing efforts for improving quality of all processing companywide. We are excited to see her thrive in this new role. Processors can look forward to hearing from her and more details will be coming soon. Congratulations Mary!

In addition, the URLA has been updated to include the Language Preference field on URLA Part 1, and the Homeownership Education & Housing Counseling fields on URLA – Lender. These fields populate the Supplemental Consumer Information Form (SCIF), which will be included with disclosures starting on March 1, 2023. SimpleNexus will capture the response to these questions on the online application – any 1003 started in Encompass will need to have these questions completed manually. A copy of SCIF form is attached.

CBC Mortgage Agency

C/O DocProbe

1133 Ocean Avenue

Mail stop code: DP7822

Lakewood, NJ 08701

Attached are both the updated Lending Guide as well as the CBC Mortgage Agency Announcement for a summary of the guideline updates.

Starting Monday, March 6th, California Housing Finance Agency (CALHFA) loans can be originated. When originating these loans please make sure that the correct loan program template is selected in Encompass.

To lock, please submit the attached CALHFA lock form to secondary by 4:30pm EST to lock same day. Loans must be conditionally approved and within 15 days of closing to lock.

We will not be offering High Balance, Homestyle, 203k, Energy efficient, or section 184 loans through the CALHFA program.

On the backend the branch will make .25% and must charge the rest in origination. At a minimum you will need to charge 2% in origination plus processing and UW fees. In total we are allowed to charge up to 3% in origination including processing and UW. Collect the max in fees to out to account for limited backend margin. Loans must still comply with ATR/QM fee limits. A $250 funding fee, $75 tax service fee, and $10 flood cert fee must be charged as well.

Please make sure that you verify your P&L can support the pay structure of this program prior to originating.

Agency Updates

Fannie Mae

Effective immediately, as Fannie Mae continues down the path of Modernization flexibilities when it comes to valuation, allowable alternatives to a 1004D Final Appraisal Inspection when there are completion or repair requirements (subject-to) in the original appraisal are implemented. Please find attached both the FNMA Selling Guide Announcement 2023-02, FNMA Selling Guide section B4-1.2-05, Requirements for Verifying Completion and Postponed Improvements, and Attestation Letters for both New/Proposed and Existing Construction.

Note: All Value accepted + PDR and Hybrid appraisals are placed with Clear Capital (via ValueLink/Appraisal Department) which is one of the five approved vendors for these products. (Did you know that 40% of the time, Fannie Mae Hybrid appraisals turn into Value Accepted + PDR at the lower cost of time?)

Freddie Mac

Bulletin 2023-5: Freddie Mac is expiring the remaining temporary COVID-19 related underwriting requirements. All Loan Product Advisor feedback messages referencing the temporary COVID-19 related requirements will be expired on May 1, 2023, but can be disregarded effectively immediately.

Bulletin 2023-6: Effective for Mortgages with Settlement Dates on and after July 3, 2023, Non-Occupying borrowers may not be an interested party to the transaction (i.e. builder, seller, real estate agent or broker).

IMPORTANT REMINDER!!! Any conventional Cash-Out Refinance utilizing Freddie Mac’s LPA is subject to a 12-month seasoning with note dates on and after March 7, 2023.

FHA

In February, we brought attention to two BIG items from FHA – Annual MIP Factor updates and 12-Month Positive Rental History impacting AUS findings. We are updating these to include the following information:

FHA Annual MIP Factors – If you select the “Get MI”, you will need to manually override the Annual MIP Factor (monthly) to the 30 BPS reduced amount. Encompass has not caught up quite yet with our awesome-ness!

FHA Positive Rental History – Below and attached are the DU Release Notes for Government Loans regarding FHA Case Assignment Dates and how this will impact your DU. “No” means that the checkbox would NOT be selected at all in our Encompass environment.

VA

GREAT NEWS for our VA eligible borrowers! Effective with loans closing on and after April 7, 2023, VA is reducing most VA Funding Fee charges. Exhibit A attached includes the current VA Funding Fee charges and Exhibit B includes the updated VA Funding Fee charges. We are including with this an updated VA Loan Limit Calculator for loans closing on and after April 7, 2023.

* * *

Upcoming Events and Reminders

If you need an invitation to one of the Zoom meetings listed below, please respond to this message or email ProductionSupport@vandykmortgage.com

FHA Disputed Derogatory

Did You Know that you MUST manually downgrade Approve/Accept classifications if the borrower has $1000 or more collectively in Disputed Derogatory Credit Accounts UNLESS the Credit is rescored to remove the dispute?

What is defined as derogatory?

We have verified with HUD whether the following statements on any disputed tradeline will need to be considered as a part of the $1000 or more:

Dispute Resolved – Customer Disputes After Resolution – YES

Dispute Resolved – Consumer Disputes After Resolution – YES

Dispute Resolved – Customer Disagrees – NO

Dispute Resolved – Consumer Disagrees – NO

IMPORTANT – You cannot supplement a disputed account to avoid manual downgrade. The Credit Report MUST be rescored.

25 Points

Wait a moment for the newsletter to load, otherwise scroll down to download a copy!

February 3, 2023

It’s less than a month away – have you finalized your Fly-in plans yet? TODAY is the deadline to sign up for your preferred breakout sessions. Please follow this LINK and sign up for your optional sessions by Friday, February 3rd. If you do not sign up by this deadline, breakout sessions will be chosen for you (don’t worry – they are ALL great options)!

Effective with loans locked February 15th and beyond the new Loan Level Price Adjusters (LLPAs) grids will be active in OB. Any loan locked prior to February 15th will need to fund by April 14th to avoid the additional LLPAs applying to the loans. See attached for formal announcement, LLPA comparison Excel, and Fannie Mae LLPAs.

With this change, we will implement a requirement for proof of property taxes (tax cert/property tax bill) to our minimum UW submission standards when there is a subject property. If a tax certificate is not available or the home is new construction, the loan can be submitted to UW if a 1.5% of appraised value factor is used to calculate property taxes.

We are now approved as a Principal Agent with FAR for Reverse Mortgages! The Reverse Team can assist you with questions, scenarios, proposals etc., and we are able to broker HomeSafe to FAR. With AAG and FAR as our two in-house PA options for reverse mortgages and the ability to offer the conventional HomeSafe loan on the broker side again, we are looking forward to seeing an uptick in volume in the coming months. Contact your VanDyk Mortgage Reverse Team (Sophie Morales, Kristine Kuss, Adam Wilson) with questions or if you need assistance!

We will soon begin including eNotes in our hybrid eClosing packages. An eNote is an electronically signed version of our Note that can be eSigned via Simple Nexus. Including an eNote will not significantly change the hybrid eClose workflow, but will take us one step closer to a full eClosing!

We have closed a handful of buydown loans and are making a minor adjustment to the closing packages for these loans:

Effective with loans locked on or after March 1: Tennessee Housing is updating their fee structure. TN Housing loans will need to have 1% origination and $1,400 in customary fees charged. On the back end, the branch will make 1% plus the 1% in origination.

Due to the implementation of the LLPA hits for DTIs over 40%, and to prevent any last-minute hiccups (such as needing to redisclose a fee increase), we are adding the Tax Bill/estimate as part of our Minimum Standards for Submission into Underwriting for any loans with a property address. If you do not have a tax bill or estimate, please use 1.5% of the purchase price or value as a default in Encompass for properties outside of Nevada. Nevada is defaulted to 1%. This will be effective for all loans submitted into Underwriting on and after Monday, February 6, 2023.

Before you email the Condo Department or submit a request for Condo Review, don’t forget to check the Condo Approval list in Howee to see if your project is already approved. If the project is on the Fannie approved list, all we need is the master insurance (we don’t even need a questionnaire). If you email the Condo Department with documentation that is not required for the review and it “opens a can of worms,” we cannot close the can without additional review and documentation.

VanDyk has contractual compensatory agreements with the lenders we broker loans to. When locking your loans, you will need to ensure the minimum compensation is met. This document will help you understand the difference between Lender and Borrower paid compensation, the two options given by the lenders in their various pricing engines. Please review Locking a Brokered Loan – Compensation, attached, for more details.

For applications dated on or after 1/31/2023, OR loans with a note date on or after 2/15/2023: 2022 W2s OR a Written VOE will be required.

We’ve also created a cheat sheet to reference when you’re looking for help calculating income on a file. Please see the attached PDF: Income Calculation Help.

Encompass has some updates slated for release on February 16th which will impact this form. We will roll out our updated Borrower Summary 2023 Encompass form and hold training sessions after this release date – watch your email for invitations and additional information.

Champions: Champions is a borrower paid-comp only outlet, but are still going to hit us with an EPO fee if a loan pays off with 180 days of funding. If you are using their Ally No Ratio program, the EPO extends to 360 days from funding. Champions wants to make it clear that their Ally product is not to be used for short term funding, which is the reason for the 360 day timeframe.

Flagstar: Flagstar updated their Doctor Program to include additional licenses/occupations in the medical field. Please see the attached Broker Update email with more details about this program!

Go Mortgage: Go Mortgage, one of our One Time Close Construction outlets, requires all team members to complete a training prior to receiving credentials to log in. To make this easier, we have scheduled two sessions with Go Mortgage that you can join in order to receive your credentials. Invitations were sent on Friday, 2/3 – if you did not receive and would like to attend, please email ProductionSupport@vandykmortgage.com

The highly anticipated day has arrived! Once your access is set up, you will be able to obtain a 1-bureau soft pull in Simple Nexus with the click of a button. Instead of accessing the Sarma website and entering borrower data manually, simply locate your borrower’s application in SN and click the “Soft Credit Check” button. Easy!

Important note: You will not have the ability to pull both soft AND hard credit within SimpleNexus – it is one or the other. Starting today, Production Support will be working through getting access to users, and will be reaching out to your branch manager once this feature is ready for your team.

Please remember: soft pulls are not imported into Encompass or used to run AUS. There is no liability report to be imported. They are not to be used for qualifying. If you have any questions, reach out to Production Support.

Just a reminder that Loan Officers have a “share” link available to get connected to realtors/agents within SimpleNexus. You can find this link under Contacts > Partners. We attached an overview of what the agent sees on the SimpleNexus side, and you can watch a demo of the Partner portal here. If you have any questions, reach out to Production Support.

If you ever run into the issue where your UDM is not monitoring, and you do not have time to wait for it to turn on and start running to meet your ECD, we have an option to provide a no FICO tri-merge “refresh” soft pull within 10 days of closing. For additional details or assistance, reach out to Production Support.

For Citi Jumbo loans and NewRez NonQM files, appraisals that come back with a property value showing “declining”/Declining Market, the maximum LTV/CLTV will be reduced by 5%. We anticipate other investors may follow suit – we will pass along updates as we receive them.

Mortgage fraud – including occupancy and income fraud – has become more prevalent over time and is a particular concern during an economic recession. Upheaval in housing markets, homeowners facing financial difficulties and unscrupulous persons looking for easy money all contribute to a climate in which mortgage fraud may occur. Current statistics indicate that 1 in every 109 mortgage applications show indications of fraud. For more details, review the “What is Fraud” attachment.

Agency Updates

Fannie Mae

Freddie Mac

FHA

VA

Upcoming Events and Reminders

If you need an invitation to one of the Zoom meetings listed below, please respond to this message or email ProductionSupport@vandykmortgage.com

35th Anniversary Events

March 2 – 4, 2023 | Annual Sales Fly-in

Occupancy Check!

Did you know that investors are being scrupulous about checking on the borrowers after closing to ensure they are occupying the home?

***

Employment Validation – Self-Employed – Fannie

Did you know you can receive Self Employment income validation in Fannie Mae’s DU when you have obtained tax transcripts from Dataverify?

Your SE income can also be validated in Freddie Mac’s LPA, if your LoanBeam is run though the Encompass interface. Awesome!

***

Credit Orders & Borrower Solicitation

As many teams are already aware, the amount of solicitation that borrowers receive after their credit is pulled has drastically increased.

It’s important to note that Sarma is not selling leads – brokers and lenders are buying leads from the bureaus. The only way to get out of not getting calls is to have the borrowers opt-out by visiting www.optoutprescreen.com or calling 888-5OPT-OUT (888-567-8688). It does take about 5 days for this to be set up.

Some teams are taking the approach of doing a 1-bureau soft pull, and then having the borrower opt-out prior to doing the hard pull. Soft pull inquiries cannot be sold.

25 Points

Wait a moment for the newsletter to load, otherwise scroll down to download a copy!

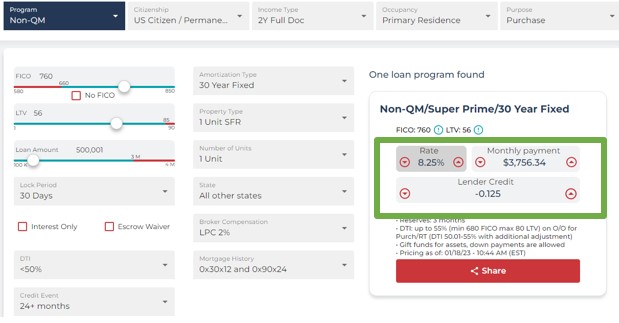

VanDyk has contractual compensatory agreements with the lenders we broker loans to. When locking your loans, you will need to ensure the minimum compensation is met. This document will help you understand the difference between Lender and Borrower paid compensation, the two options given by the lenders in their various pricing engines.

Borrower- Paid:

The compensation to the broker (VanDyk) is paid at closing on the CD by the borrower. The fee (usually between 2-2.75%) is collected as a broker compensation fee on the Closing Disclosure in addition to the Lender’s fees.

In this example from A&D, the interest rate quoted is 7.49% with the borrower paying the broker’s compensation. The borrower will be charged 2% on the CD for this transaction.

Lender- Paid:

Using the same scenario, we change the compensation to Lender Paid. This means the 2% compensation paid to VanDyk is built into the interest rate and paid by the Lender (A&D) to the broker (VanDyk) and not collected on the CD. The interest rate is 8.25% instead of 7.49%.

It is important to understand that the total compensation being locked in is not the end LO compensation amount, but the amount the lender will deliver to VanDyk Mortgage from which all the expenses will be deducted from (Branch Comp, LO Comp, Processing fee, etc.).

When you submit the Brokered Loan Request in Encompass, you will need to ensure to enter the compensation type and amount (%) are entered:

If you have questions or need help locking in a brokered loan, please contact ProductionSupport@vandykmortgage.com

DYK? For FHA – whenever the 4000.1 Handbook doesn’t specify a time frame, it can be assumed that it’s from the case number assignment date.

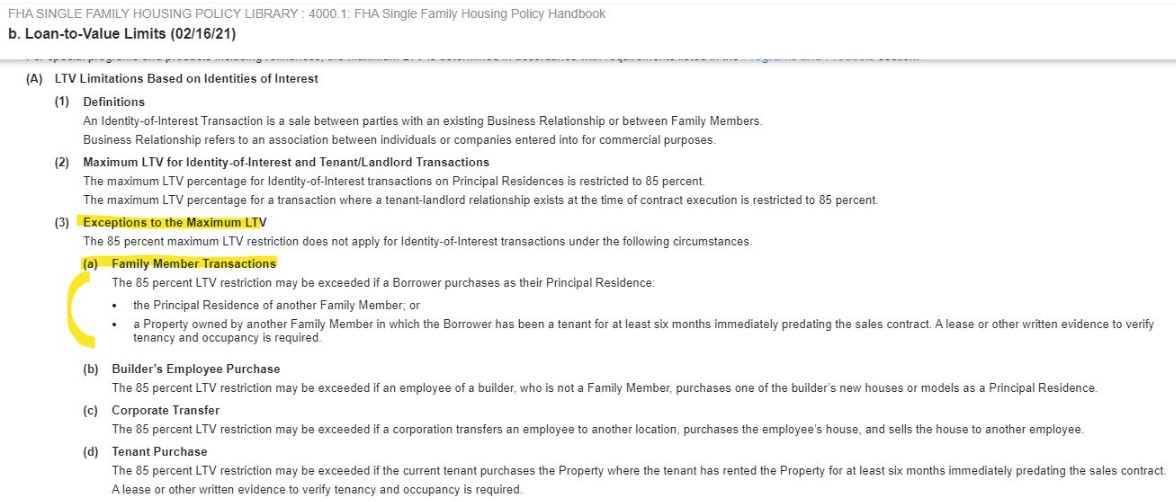

DYK – For FHA, when you have a Gift of Equity, there is an automatic identity of interest as only “family” may give a Gift of Equity. You will need to document the identity of interest appropriately or your LTV will be limited to 85%.

January 6, 2023

Have you seen Lindsey Kuhnle’s DYK posts in the VanDyk Happenings Facebook group yet? If you missed them, we’ve created a Howee’s Helpful Tips blog category at VDMC.net to collect all of the knowledge that is shared. Check it out!

QC Review Process: Effective Jan 1, non-government brokered loans will be reviewed by Production Support for completeness. The QC department will continue to review government loans. Files should be moved to the resubmittal milestone only when the loan has closed and funded, and the entire closing package with all loan documents, approvals and a copy of the broker check have been uploaded to the Encompass file.

REMN HELOC: Although the borrower completes the application for this loan with REMN via their website, VanDyk requires an Encompass file and secondary approval to broker like any other loan. Be sure to follow the normal procedure to obtain approval to broker this product or any other loan.

QUESTIONS, SUPPORT & TRAINING: As a reminder, please reach out to Production Support for any broker questions – we are also able to provide training at a branch level for specific broker processes.

With aggressive interest rates, we have determined there is a need for a more relaxed review to lock our JUMBO customers into their interest rate more quickly. Upon request to the JUMBO Team for approval to lock, we will be doing a scrub to verify that the loan appears to meet the specific jumbo investors requirements. This will not be a full review or approval of the loan file, only the approval to lock, and any areas of concerns will be expressed. The loan will not be fully underwritten until it is submitted into underwriting.

As a reminder, we must underwrite to our specific JUMBO investors guidelines and overlays.

Email: JumboLoanReview@vandykmortgage.com

With many economists predicting that we could see a refinance market in the next 8-16 months, we wanted to remind every one of our commissions earned policy (Early Payoff). Please see the attached for a refresher on the policy. We do have a pipeline view in Encompass called “Recapture Pipeline” that is available for LOs to search loans and get an estimate for when a particular loan is in the clear. If you have a situation where you might be close on recapture or just want a further look at the scenario, reach out to secondary and they can dive deeper into the exact loan scenario and investor policies to ensure we have an exact date.

Chenoa has made the following update, effective January 1, 2023. Matrix and updated guide are attached.

On December 23rd Secondary put out the attached “FHFA Updates in Optimal Blue.” If you missed it, please read! If a borrower meets the below two requirements on a Conventional transaction they are eligible for no LLPA’s.

Effective January 1, 2023, MSHDA will require federal returns for tax years 2020, 2021 and 2022 on all new MCC submissions. The completed MCC-004 Income Tax Affidavit is to be submitted in place of the 2022 federal tax return up until February 15, 2023. After February 15, 2023, the 2022 federal tax return is required to be submitted with every MCC file before a Commitment can be issued. This applies only to the Mortgage Credit Certificate (MCC) program.

A new Title Request Form for Manufactured Homes is now available in Encompass. This form gives additional guidance to Title Companies on what will be needed for us to close on a manufactured home. Please use this form for all title orders on Manufactured Homes.

The Encompass input form Borrower Summary – 2021 will soon be replaced with an updated version, Borrower Summary – 2023. It will feature new fields for the Credits and Adjustments as well as an updated second input form (Page 2) for disclosure questions and fee rule overrides.

The form update will effective 1/16/23. Trainings on the new form will be provided before and after the change.

We have been approved with CALHFA but must undergo extensive training before they will allow us to originate. If you plan to originate CALHFA loans, please register for Part 1 and 2 of Sales and Ops training using the links below. We will issue another announcement once we are fully ready for launch.

Don’t miss the Newscast on Friday, 1/13 – Brad, our VP of Secondary and Capital Markets, will be joining us to recap his 2022 year-end commentary. He’ll also share any updates that have arisen since. If you missed the commentary, find the email attached!

Agency Updates

Upcoming Events and Reminders

If you need an invitation to one of the Zoom meetings listed below, please respond to this message or email ProductionSupport@vandykmortgage.com

35th Anniversary Events

March 2 – 4, 2023 | Annual Sales Fly-in

VDM Newscast Dates

Just a reminder that the VanDyk Mortgage Newscast will be held on the second Friday of each month for 2023.

Invitations were sent in December, please let Production Support know if you need it re-sent!

***

Reminder: Self-Employment and Rental Income Support Team

As a reminder, the Self-Employment / Rental Income Support Team is not designated for JUMBO loans.

Please continue to submit all jumbo loans through the Jumbo Loan Review Team at jumboloanreview@vandykmortgage.com.

Instructions for requesting support are attached.

***

Video Portal

Did you miss an Iron Sharpens Iron or a Newscast? Don’t worry – those recordings are available on VDMTube here!

***

Product Matrices

You can find our VanDyk Mortgage product matrices by asking Howee, or by going directly to the Shared Files – in the Product Matrices folder.

***

Sales Fly-In – RSVP Reminder

Our 2023 Sales Fly-In is March 2nd – March 4th! If you already RSVP’d, thank you! If you haven’t and plan on attending, what are you waiting for?!

RSVP today: https://2023-VDM-Sales-Flyin.eventbrite.com

25 Points